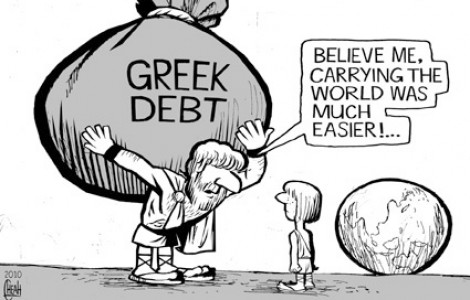

A join EU Commission/ECB/IMF report says that Greece will be unable to meet its target of getting national debt down to 120% of GDP by 2020 even if it implements all of the EU's austerity demands.

In order to get the promised EU/IMF payday loan, the Greek government needs to agree a 70% write-off with its private creditors. Apparently this will take four weeks to arrange and Greece needs €14.5bn of someone else's money to service its debts on the 20th of March. That means a bailout loan has to be agreed no later than Tuesday to give the Greek government the 28 days it needs to negotiate the 70% write-off.

The EU was supposed to have agreed the bailout loan on Wednesday but they decided to make Greece wait until Monday for a decision. The most likely reason earlier in the week was that they would try and screw more concessions out of the Greek government because Greece getting the bailout loan was believed to be a foregone conclusion but Schäuble's comments and the EC/ECB/IMF report cast doubt on that theory. Could they be holding back because they're genuinely unsure whether they should let Greece fail?

Apparently, US banks are already preparing for a Greek default and if the rumours are to be believed, Greece is being managed into default. If they do default and crash out of the €uro there won't be many Greeks complaining. They've seen prices go through the roof since the Drachma was replaced, interest rates pegged unacceptably high to suit the Franco-German Empire and now devastating EU-imposed austerity measures when they're in trouble.

Greece should have left the €uro before things got out of hand. Without wanting to sound like a broken record where Iceland is concerned, they have really set the bar for economic recovery. They're forecasting a budget surplus next year and Fitch have just upgraded their credit rating to investment grade, citing their "unorthodox crisis policy" as the primary reason for their recovering economy. The "unorthodox crisis policy" involved letting its banks fail, prioritising their own citizens over foreign investors, reducing interest rates and imposing restrictions on foreign currency transactions - none of which is an option to Greece while it's in the €uro.

Stuart Parr is a

Stuart Parr is a